"Managing money is more important than making money"

Brief

Young adults and students often lack healthy financial habits, leading to difficulties in managing their finances effectively. Many struggle with tracking expenses, budgeting, and setting financial goals, resulting in financial stress and poor decision-making. This gap in financial literacy and practice can have long-term negative impacts on their financial well-being and mental health.

SOLUTION

The Solution is to create a mobile app that empowers young adults and students to take control of their financial future. By offering intuitive tools for tracking expenses, creating budgets, setting financial goals, and engaging in savings challenges, the app will make financial management accessible and even enjoyable. The impact of this solution will be profound, equipping the next generation with the knowledge and confidence to manage their finances effectively, reducing financial stress, and promoting long-term financial well-being.

What I did

I employed a variety of research methods to deeply understand the challenges faced by students and young adults in managing their finances. This included:

01 Competitive Analysis

To outline the strengths and weaknesses of the competitors compared to those of my own research.

02 Workshops

To engage users in interactive sessions, helping to identify common financial difficulties and brainstorm potential solutions.

03 Online Surveys

To gather quantitative data on financial habits and challenges.

04 User Interviews

To gain qualitative insights into the personal experiences and pain points of the target audience.

05 Card Sorting

To understand how users categorise and prioritise financial tasks and information.

06 Wireframes

To define what content goes where, the flow of how users will move through the product, and overall layout.

07 Prototypes

Created prototype with enough features to allow the users to test it and offer feedback.

08 Usability Testing

To spot usability issues and any other roadblocks that users may encounter.

Timeline

Competitor Analysis

Mint

Mint is a personal budgeting app from Intuit with a free and paid version. Launched in 2006, it’s one of the most popular budgeting apps available today, allowing users to manage all their financial accounts in one place. Customers praise Mint’s user interface, which features bill alerts, custom budgets and the ability to set specific savings goals.

Pocket Guard

PocketGuard is a budgeting app that lets you set a custom budget and track your transactions, showing you how much spendable cash you have while reminding you about any recurring payments. Additional features like bill negotiation and spending insights make it helpful for anyone who wants to set a custom budget, pay off debt, lower their bills, reduce spending or work toward savings goals.

Honeydue

Budgeting with a partner can be stressful, but Honeydue can help make money conversations easier. Designed especially for couples, Honeydue is an interactive app where two people can manage household expenses together.

Good Budget

Goodbudget is a budgeting app that relies on the traditional envelope system to help users budget their monthly expenses. This app is a great fit for consumers who want to organise their priorities and get ahead financially.

YNAB

You Need A Budget, or YNAB, as it is often called, is a popular budgeting app designed to help people take charge of their finances. Launched in 2004, YNAB not only allows individuals to create a budget but also can help you save money. According to YNAB, the average new user saves over $600 in the first two months of use and $6,000 in the first year alone.

I have conducted a competitive analysis, gathering data on a range of existing products in the market. This secondary research has enabled me to identify areas where user needs are not being adequately met by current offerings, revealing opportunities for innovation and differentiation.

Building on this analysis, I further explored user preferences and pain points through in-depth research. This involved gathering primary data through interviews, surveys, workshops to gain a deeper understanding of users' needs, behaviours, and motivations.

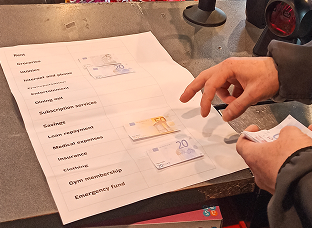

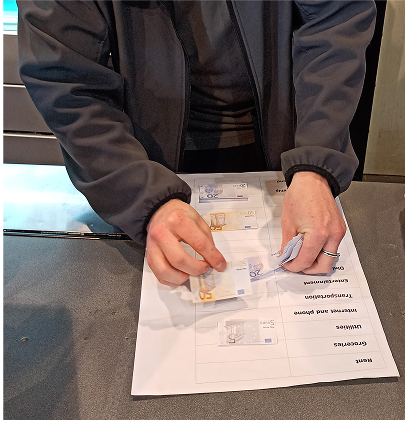

Workshop : Expenses Tracking

Conducted expense tracking workshop Individually and also on focus group.

Users

Students and young adults.

Goal

- To Know their thoughts and understandings on spending habits, saving goals.

- To know if participants track their expenses and how do they do it?

Workshop

The workshop was asking participants how much would they spend in a month. Give the x amount of money (Fake currency/Toy currency) and a sheet with a list of expenditures. Ask participants to distribute money on the list of expenditures. There is a credit card option for who has ran out of the money.

Findings

-

Most participants didn’t track expenses regularly.

-

Financial goals, such as savings or debt repayment, were common but poorly executed.

-

Overspending on non-essentials was frequent, leading to missed savings opportunities.

-

Mental budgeting was the predominant approach, which lacked accuracy.

Surveys

I conducted surveys to gather quantitative and qualitative data on users opinions, knowledge over time.

Insights from Surveys

76.5%

Confident in using digital financial tools

23 out of 34 are confident in using digital financial tools, a small portion still rely on manual expense tracking.

88.2%

Positive opinions on money management model

Nearly 9 out of 10 are interested in using money management models like budgets or savings plans.

76%

Setting financial goals

Over 23 out of 34 are interested in setting financial goals within the app.

Room for Improvement in Financial Awareness

Only 1 in 9 users (11.8%) currently review their income and expenses regularly.

User Interiews

Conducted extensive face to face interviews to learn what user experiences are like, their behaviours, needs, value, and desire.

Focused on Past Behaviour vs. Hypothetical Scenarios

1. Tell me about the last time you tried to stick to a budget. How did it go?

2. Can you recall a time when you faced a financial emergency? How did you handle it?

Open-Ended Questions

3. What strategies do you currently use to save money?

4. Walk me through how you check your financial status.

Mitigating Own Biases and Presumptions

4. How do you decide when to make a purchase?

5. What do you like or dislike about tracking your expenses?

Follow-up Questions

6. Have you tried any apps for tracking expenses?

7. What was your experience?

8. Would automatic tracking make a difference for you?

9. How often would you check your spending report?

10. When was the last time you felt financially in control? What made the difference?

11. Have you ever tried setting financial goals? What worked or didn’t work?

12. How do you usually react when you realise you've overspent?

13. If you could improve one part of your financial habits, what would it be?

14. What would motivate you to regularly check your financial health?

Key Insights from Interviews

User Goals

- Easily track spending without too much effort

- Build better savings habits for future financial security

- Avoid stress and financial surprises

- Stay motivated and engaged with budgeting tools

Pain points

1. Users rely on mental budgeting, which is unreliable.

2. Users adjust only after overspending or facing an emergency.

3. Saving is goal-driven, Users save more effectively when they have a specific target.

4. Financial apps can be overwhelming, Users quit due to complex features and lack of useful insights.

Key findings

-

Finance tracking tools should be simple and intuitive.

-

Budgeting tools must be adaptable to individual goals and lifestyles.

-

Stress cause to increase impulse purchases

Potential Areas for Design Intervention

Archetype

Overview

A tech-savvy, impulsive spender who enjoys life’s little indulgences but struggles with consistent financial discipline. They respond well to engaging, gamified financial tools that help them save without feeling restricted.

Journey Map

Ann wants to save money to fulfill her financial goals but is not able to save a cent. She gets a challenge notification from an app. She wants to try and see if she can complete the challenge and save some money.

User Flow

This flowchart illustrates the steps a user takes from home to accessing the main features of the app.

Information Architecture

Card Sorting

Utilised card sorting to understand information organisation preferences for 1. Basic Budget Planning 2. Home Screen

For Basic Budget Planning

I gave users a board and post It’s. The board contains a table with 3 headings:

1. Needs

2. Wants

3. Savings

and asked users to write all their needs, wants and savings goal.

Output

Based on this card sorting, more options are added and prepared a basic budget plan.

For Home Screen

I used open and closed sorting. I gave users some basic section cards to organise and also asked them to add new sections of their interest.

Output

Based on this card sorting, I prepared home screen and its content.

Ideation

Low-fidelity Wireframes & Testing

Feedback

Based on my research findings, I created low-fidelity wireframes to test whether the content structure aligned with the insights gathered.

I then tested these wireframes with users to see how well the insights were implemented. While the feedback was positive, users found it difficult to provide detailed input since low-fidelity wireframes lack visual clarity and interactivity.

Mid-fidelity Wireframes & Testing

Feedback

After incorporating initial feedback, I iterated on the designs and developed mid-fidelity wireframes. I then conducted usability testing, which yielded positive responses from users. They appreciated the information layout and found the navigation intuitive and easy to use. The overall flow felt simpler and more structured compared to the low-fidelity version.

Hi-fidelity Wireframes & Testing

Feedback

Following the usability testing of mid-fidelity wireframes, I moved on to designing high-fidelity screens. I focused on refining visuals, incorporating colours, icons, and illustrations to create a more aesthetic and engaging experience.

Once the hi-fi screens were ready, I conducted another round of user testing. The response was overwhelmingly positive users appreciated the design, clarity, and visual appeal. They found the final version both functional and enjoyable to use.

Identified a roadblock

Problem

Core features can help users in their financial journey. But how to make Students and Young adults engage with these features and build health financial habits?

Solution

To Introduce gamified savings challenges paired with friendly, motivational notifications to make savings fun and engaging.

How

Behaviour Can Be Designed

Core Concept development: Gamification

Design Principles Applied

User-Centred Design

Focused on addressing user pain points and behavioural patterns.

Behavioural Finance

Behavioural finance combines psychology and finance to study how cognitive biases and emotions influence financial decisions. It explores the psychological factors that impact individual’s financial behaviour and decision-making processes.

Hook Model

Incorporated habit-forming design to encourage regular app use. The Hook Model is a methodology that can be used for addictive services or products which the users will come back to again and again. The main aim of the model is to create a customer habit. This is done by creating a link between the customers’ problem and the solution which offers and reinforces it through repeated exposure to the product.

Gamification

Implemented challenges and notifications to motivate and sustain user engagement.

What & How

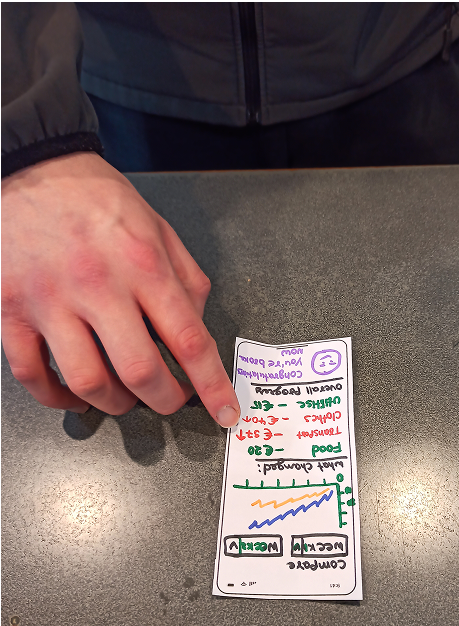

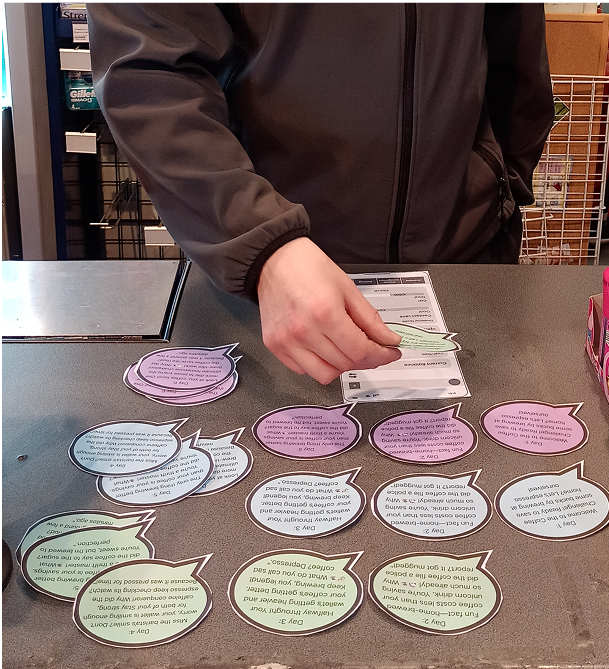

Workshop: Coffee Challenge

I conducted a 7-day coffee challenge to test the effectiveness of different notification tones. The challenge used three distinct tones:

-

Professional and Motivational

-

Witty and Humorous

-

Friendly and Encouraging

During the workshop, most participants struggled to complete the challenge. When asked about their experience, they shared that they liked the concept of notifications paired with challenges, but found a 7-day challenge too difficult for beginners. They felt that a shorter challenge (3 days) would be easier to complete.

Taking this feedback into account, I reduced the challenge duration from 7 days to 3 days and conducted the workshop again with the same participants. This time, everyone successfully completed the challenge.

When asked about the tone of the notifications, the majority found the Friendly and Encouraging tone the most comfortable and motivating.

Output

By combining gamification, psychology, and behavioural design, this system helps young adults form better financial habits in an effortless, enjoyable way. Through a mix of challenges, engaging notifications, and habit-forming strategies, financial management becomes a fun and sustainable part of their routine.

Impact

- Users reported greater awareness of spending habits

- Encourages financial discipline through positive reinforcement

- Helps users form long-term habits by breaking goals into manageable steps

- Increases daily app engagement

Story Board

The storyboard illustrates how gamified challenges and engaging notifications can help users build better financial habits in a fun and motivating way.

Explanation

How Challenges and Notifications Work, the idea is simple:

Small, achievable challenges combined with timely, engaging notifications encourage users to rethink their spending habits. Instead of enforcing strict rules, this method makes saving enjoyable, rewarding, and effortless.

1. User's Initial Struggle

The story starts with the user realising that they spend too much money and want to develop better saving habits but struggle to control their spending.

2. Challenge Invitation via Notification

The user receives a friendly, intriguing notification that introduces a small challenge, eg: “Skip coffee for 3 days and save €10.” This simple goal feels achievable and fun, making the user curious and willing to try.

3. Daily Encouragement & Reminders

Each time the user feels tempted to buy coffee, a humorous and encouraging notification reminds them about the challenge. The playful tone helps the user resist the urge without feeling pressured.

4. User Progress and Engagement

The user actively marks their progress in the app after skipping coffee each day. This creates a sense of achievement, reinforcing the habit.

5. Final Reward & Motivation Boost

Upon completing the challenge, the user receives a congratulatory message that celebrates their success. This provides positive reinforcement, making them feel good about their decision. Seeing real savings (€10) encourages the user to take on more challenges, gradually improving their financial habits.

Style Guide

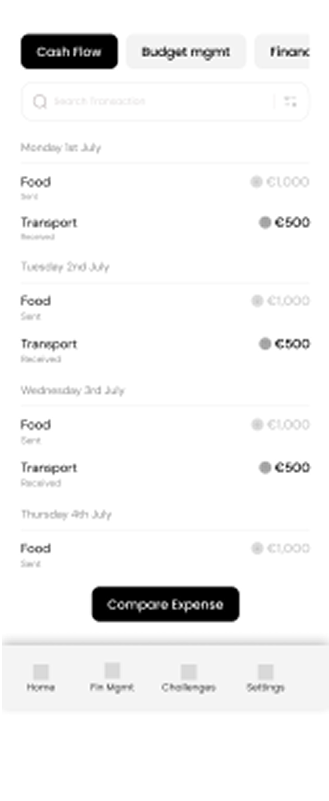

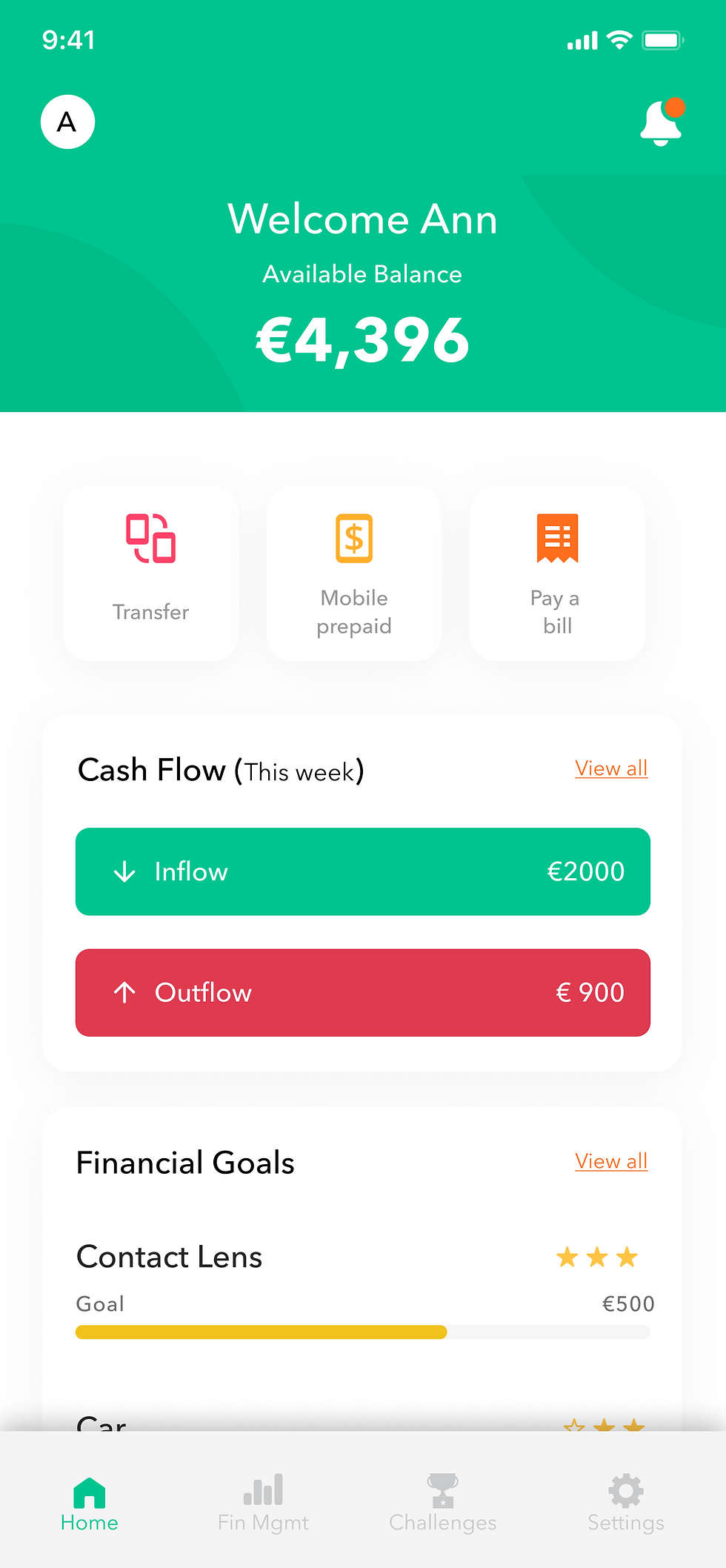

Cash Flow

Users can effortlessly track their daily expenses and gain insights into their spending patterns. The app allows them to compare their current expenses with past spending, helping them identify trends and make informed financial decisions. A visual progress tracker gives users a clear overview of their financial habits, enabling them to take control of their cash flow.

Budget Management

Users can choose from various budget models and input their preferred spending limit. The AI-powered system will then generate a personalised budget plan based on their past expenditure. This tailored approach ensures that budgeting is realistic and achievable. Additionally, users have full control to customise their budget according to their unique needs, making financial planning more flexible and effective.

Financial goals

Users can set financial goals and prioritise them based on urgency or importance, whether it's saving for a vacation, paying off debt, or purchasing something significant. The app seamlessly integrates savings with goals, allowing users to allocate their saved money towards achieving these milestones. A progress tracker provides motivation and a sense of accomplishment as users move closer to their financial targets.

Smart AI Notifications

AI-driven notifications serve as friendly reminders and motivators, encouraging users to stay on track with their financial habits. These notifications go beyond standard alerts, they introduce fun and interactive challenges, making the process of saving money more engaging. By blending encouragement with practicality, the app helps users form sustainable savings habits in an enjoyable way.

Challenges

Based on user's spending patterns, the AI generates tailored savings challenges to encourage better financial habits. These challenges come in varying difficulty levels, starting with small, achievable tasks and gradually increasing in complexity. Once a challenge is completed, the money saved is automatically added to the user’s financial goals, reinforcing positive behavior. By gamifying the savings experience, the app makes financial discipline more rewarding and enjoyable.

Social Impact

Improved Financial Literacy:

Users developed better spending and saving habits

Reduced Stress:

Easy-to-use tools alleviated financial anxiety

Long-Term Benefits:

Empowered a generation with tools to achieve financial stability.

Takeaways

What Went Well:

- Gamified challenges and notifications were effective in habit formation.

- Iterative design ensured alignment with user needs.

Challenges Faced:

- Balancing simplicity with feature richness.

- Balancing engaging notifications with avoiding annoyance was a delicate process.

Future Improvements:

- Introduce milestones and rewards to further gamify the experience.

- Explore AI-driven insights to offer personalised financial advice.